Car Finance Check Before Buying: Step-By-Step UK Guide

Don't buy a car with hidden debt. Use our UK guide to run a car finance check before buying, verify V5C logs and VIN details to ensure a safe purchase.

Car Finance Check Before Buying: Step-By-Step UK Guide

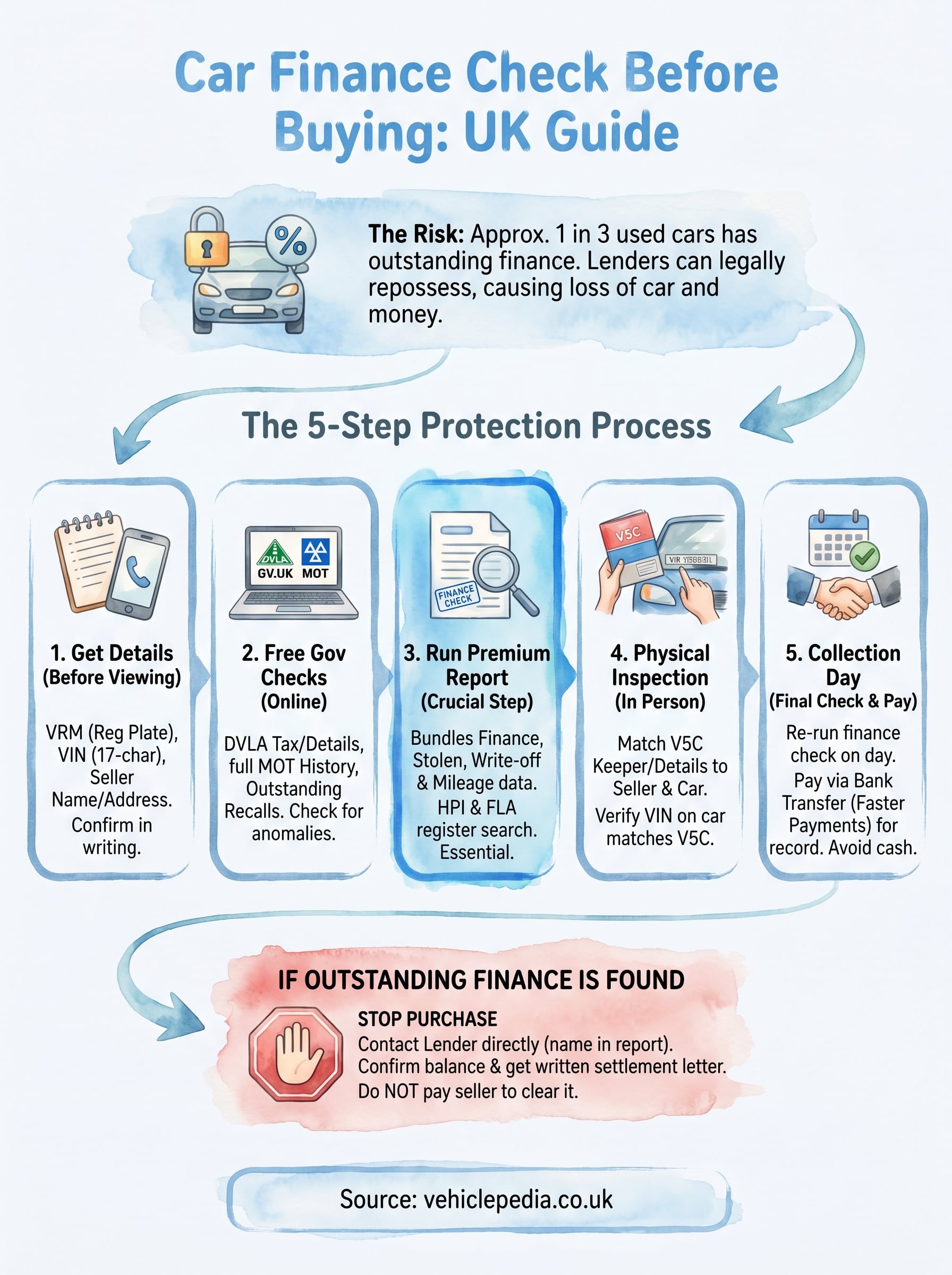

About one in three used cars on the UK market still has finance owing on it. Buy one without checking, and the finance company can legally take the car back, leaving you without the vehicle and without your money. Running a car finance check before buying is the single most effective way to protect yourself from this risk.

The trouble is sellers don't always tell you about finance agreements. Some don't even realise the debt is still there; others hide it on purpose. Either way, it's you, the buyer, who carries the consequences. Without a proper check, there's no reliable way to tell whether a car is genuinely free and clear just by looking at it or reading the V5C logbook.

This guide takes you through exactly how to check for outstanding finance, what the results actually mean, and what to do if finance turns up. We've also covered the wider checks worth running alongside a finance check, so you don't get caught out by other costly problems like stolen vehicles or write-offs. At Vehiclepedia, we offer premium vehicle history reports that include finance checks pulled from official UK databases, backed by a £30,000 data guarantee for non-trade users, so you can buy with confidence instead of crossed fingers.

What a car finance check actually confirms

A finance check searches official financial registers to determine whether a lender has a legal interest in a vehicle. When someone takes out a hire purchase (HP) or personal contract purchase (PCP) agreement, the finance company technically owns the vehicle until every payment has been made. That ownership interest is recorded on credit and asset registers. A car finance check before buying queries those registers using the car's registration number and returns a clear result: finance outstanding, finance satisfied, or no record found. Understanding what that result covers and what it does not is just as important as knowing how to run the check in the first place.

If finance is outstanding, the lender's ownership claim follows the vehicle, not the seller. You could lose the car even if you paid a fair market price in good faith.

What the check searches and what it reveals

The main database a finance check queries in the UK is HPI (Hire Purchase Information), which is managed by Experian. Alongside HPI data, reputable history report providers also search Finance and Leasing Association (FLA) records and other credit asset registers. Together, these sources hold records of the vast majority of finance agreements ever taken out against UK-registered vehicles.

A result confirms four things: whether finance is currently active, the type of finance product (HP, PCP, or conditional sale), often the name of the lender, and whether any past finance has been settled or satisfied.

Here's what each result means in practice:

| Result | What it means | What you should do |

|---|---|---|

| No finance found | No active lender interest recorded | Proceed, but still verify the V5C and VIN |

| Finance outstanding | Lender still owns the vehicle | Do not buy until the seller clears the finance |

| Finance satisfied | Previous finance was repaid and released | Safe to proceed; ask for written confirmation |

| Data insufficient | Not enough detail to confirm a clean result | Request a full report with additional data points |

What a finance check does not cover

A finance check only confirms what's registered on the databases it queries. Personal loans taken out against a car rather than through a vehicle finance product often won't appear, and informal lending between private individuals never will.

It also won't tell you whether the car has been written off, reported stolen, or has tampered mileage. Those sit on separate registers entirely, so a finance check alone leaves real gaps in your due diligence.

That's why the reliable approach is a full vehicle history report that bundles finance, stolen vehicle status, write-off category, MOT history, and mileage verification into one lookup.

What you need before you start

Gathering the right details first saves time and prevents gaps. Run a car finance check before buying without complete information, and you risk querying the wrong vehicle or missing a red flag.

The information you need to gather

The registration plate is essential, it anchors every database query to a specific car. Also note the VIN, a 17-character code stamped on the car and printed on the V5C, which confirms the plate hasn't been swapped onto a different vehicle.

Note down the seller's full name, address, and phone number too. For private sales, cross-check their name against the V5C keeper section. For dealerships, get the business name and Companies House number to verify the trader is legitimate.

Here's a quick checklist to have ready before you start:

- Full registration plate (e.g., AB12 CDE)

- VIN or chassis number (17 characters)

- Seller's full name and contact details

- Seller's address (should match the V5C keeper address for private sales)

- The asking price (useful context if results show red flags)

- Your payment method details ready for any premium report purchases

What to budget for the checks

Free checks from the DVLA and DVSA cover tax status, MOT history, and basic vehicle data, but not finance or stolen vehicle records. A full premium history report, covering finance, stolen, write-off, and mileage data, typically costs £5 to £20.

Spending £15 on a full history report before handing over several thousand pounds is one of the most cost-effective decisions you'll make in the entire buying process.

Treat that cost as non-negotiable. If a seller pressures you to skip checks or rushes the timeline, treat it as a warning sign and walk away.

Step 1. Get the right details from the seller

Incorrect or incomplete details produce unreliable results, and sellers reluctant to share basic facts are telling you something. Contact the seller before arranging a viewing and get these details in writing first, so anything that contradicts later is on record.

What to ask the seller directly

Start with the registration plate and the VIN, stamped on a plate near the base of the windscreen and printed inside the V5C. Ask the seller to photograph both before the viewing. If the plate doesn't match what they quoted, get a detailed explanation before proceeding.

A seller who refuses to share the VIN before a viewing is giving you a concrete reason to walk away before you spend time or money on the visit.

Also ask how long they've owned the car and whether they're the registered keeper on the V5C. If not, ask why in writing. And ask directly whether any finance is currently attached to the vehicle. A straightforward seller will answer without hesitation.

A template for your initial enquiry message

Use this message template when you first contact a seller to request the details you need to run a car finance check before buying:

Hi [Seller Name],

I'm interested in the [Make / Model / Year] you have advertised. Before I arrange a viewing, could you confirm the following:

1. Full registration plate2. VIN / chassis number (17 characters)3. Your name as it appears on the V5C4. How long you have owned the vehicle5. Whether any finance is currently outstanding on the car6. Whether the car has ever been written off or reported stolen

I will be running a full vehicle history check before visiting, so accurate details are important. Thank you.

Save the seller's full response before your viewing. If any answers change between conversations, note the discrepancy and raise it directly when you meet, because inconsistencies at this early stage are rarely accidental.

Step 2. Verify the car on DVLA, MOT, and recall data

These free government checks cost nothing and take under ten minutes, and you should run them before you carry out a car finance check before buying. The results tell you whether the car is legally taxed, what the recorded mileage history shows across every MOT test, and whether a manufacturer safety recall is still outstanding. Doing this before you visit the seller means you turn up with verified facts instead of relying on the seller's word.

Check DVLA tax status and vehicle details

The DVLA's free online vehicle enquiry tool at gov.uk lets you enter any UK registration plate and pull back the tax status, MOT expiry date, and basic vehicle specification within seconds. Cross-check the make, model, colour, and engine size against what the seller advertised. Any mismatch in the registered colour or engine size deserves a direct explanation from the seller before you go any further.

If the DVLA shows the car as untaxed and the seller claims otherwise, treat the DVLA record as accurate until the seller provides documented proof.

Also confirm the date of first registration shown by the DVLA. Sellers sometimes misstate a car's age when the registration year sits close to a plate change, so this thirty-second check confirms the car is really as old, or as new, as the seller claims.

Review the full MOT history

Run the car through the DVSA's free MOT history checker at gov.uk, which lists every test result and advisory notice logged since 2005. Look closely for these specific patterns:

- Recurring failures on the same component across multiple tests, pointing to a persistent mechanical fault

- Mileage anomalies where the recorded odometer reading drops between tests, a strong sign of clocking

- Repeated advisory notices that show up on several tests but were never fixed

- Large gaps between tests that don't line up with a declared SORN period

Check for outstanding safety recalls

Check the DVSA vehicle recalls checker at gov.uk for any open manufacturer recall attached to the vehicle. An outstanding recall doesn't automatically rule out buying the car, but it does confirm the repair hasn't been done. Ask the seller for the dealership invoice proving the recall work was completed, and treat a failure to produce it as grounds to negotiate or walk away.

Step 3. Run a finance and history check with the reg

Once you've confirmed the registration plate and VIN with the seller, you're ready to run the full vehicle history report. This is where a car finance check before buying earns its keep, because it searches the financial registers that government tools never touch. A full report from a reputable UK provider pulls finance data, stolen vehicle checks, write-off category records, and mileage verification into a single result tied to the registration plate you enter.

How to run the check

The check takes under five minutes. Enter the registration plate into the history check tool, confirm the vehicle details shown match what the seller described, then choose a full premium report rather than a basic free lookup. Free lookups give you limited data and usually exclude finance and stolen vehicle records, which matter most at this stage.

Follow this sequence:

- Enter the full registration plate (e.g., AB12 CDE) into the search field

- Check that the make, model, and colour match the seller's listing before proceeding

- Buy and download the full premium report, not a partial free summary

- Save the report as a PDF so you have a timestamped record

Run the check close to your viewing date rather than weeks ahead, because finance records can change status between when you check and when you hand over money.

At Vehiclepedia, our premium reports pull from DVLA records, police databases, and insurance registers, and come with a £30,000 data guarantee for non-trade buyers, giving you documented protection if something in the data gets missed.

How to read your results

Once the report loads, check the finance status section and the stolen vehicle flag first. Both are pass or fail, with no grey area. If finance shows as outstanding, stop the purchase immediately and contact the lender named in the report before doing anything else.

Then work through the remaining sections in order: write-off category, mileage consistency, and number of previous keepers. Cross-check the mileage figures against the MOT history from Step 2. Any mismatch between the two sources points to a tampered odometer, and that alone gives you solid grounds to walk away.

Step 4. Inspect the V5C and match the VIN in person

Your finance report and government checks build a strong picture, but no digital check replaces physically verifying the car in front of you. The V5C logbook and the VIN stamped on the vehicle are your two main tools for confirming the car you're buying is exactly what it's claimed to be. Fraudsters can clone a registration plate or present a V5C belonging to a completely different vehicle, so matching physical identifiers against the documents in your hands is a step you can't skip.

How to read and verify the V5C

The DVLA issues the V5C, and it holds all the official details about the vehicle. When you look at it in person, check that the registered keeper's name and address on the V5C match the seller's identity documents exactly. If the seller's name isn't the one listed as registered keeper, ask for a written explanation before going any further.

Also verify the following details directly against the car:

- Make, model, and colour match exactly (even minor colour discrepancies are worth raising)

- Engine size and fuel type align with the V5C entry

- Date of first registration matches what the seller advertised

- Number of previous keepers is consistent with the history report you ran in Step 3

- The document looks like an official DVLA-issued V5C, with a watermark visible when held up to light and no signs of uneven printing or alteration

A legitimate V5C will feel like quality paper stock with a visible watermark. If the paper feels thin or the print looks misaligned, treat it as a potential forgery and walk away.

How to locate and check the VIN physically

The VIN is stamped in at least two locations on every vehicle: on a plate at the base of the windscreen on the driver's side, and on the bodywork, typically inside the engine bay or on the door sill. Compare both locations and confirm the number is identical across each. Then compare that number against the VIN printed inside the V5C to confirm all three references agree.

Verifying the VIN physically matters because a cloned vehicle returns a clean finance result for the plate it displays while hiding the car's true identity. If the VIN on the vehicle differs from the V5C in even one character, stop the purchase immediately and report it to your local police.

Step 5. Recheck and pay the safe way on collection day

A finance agreement that showed as satisfied when you first ran your car finance check before buying can change status if the seller takes out a new agreement before collection day. A fresh check costs the same as the first one and takes under five minutes, so run it anyway.

Run a second finance check on the day

Don't rely on the report you ran days or weeks earlier. Finance records are live, so enter the same plate into the lookup tool on the morning of collection and confirm it matches your earlier result. If anything's changed, stop the handover and get a written explanation from the seller before transferring funds.

A fresh check on collection day is the last line of defence between a clean purchase and an expensive legal dispute.

Also recheck the VIN on collection day against your saved report: windscreen plate, engine bay stamp, and V5C entry should still all agree.

How to pay safely

Never pay in cash. It leaves no transaction record and no route to dispute the purchase later. For private sales, use bank transfer, ideally Faster Payments rather than CHAPS unless the price exceeds £250,000, since it settles immediately and leaves a reference number. Call your bank to verbally confirm the seller's account details before sending anything, as account fraud targeting car buyers is a real and active risk in the UK.

For dealership purchases, pay by debit or credit card where possible. Credit card payments over £100 carry Section 75 protection under the Consumer Credit Act 1974, giving you a direct claim against your card provider if the car turns out to be misrepresented.

What to do if you find outstanding finance

Finding outstanding finance doesn't automatically end the deal, but it does mean stopping immediately and taking specific steps before paying. The finance company holds a legal interest until the debt is settled, so buying now puts you at risk of repossession, regardless of how fair the price was or how good your intentions were.

Contact the lender named in the report

Contact the lender directly, quoting the registration and VIN, and ask them to confirm the outstanding balance and account status. Don't take the seller's word that finance is "nearly paid off." Lenders only release their interest once full payment has cleared, and a seller's verbal assurance carries no legal weight.

When you contact the lender:

- Quote the full registration and VIN to locate the record

- Ask for written confirmation of the outstanding balance

- Ask whether they'll accept a direct settlement payment from the sale proceeds

- Request a settlement letter once payment is confirmed

Keep every communication with the lender in writing, so you have a documented trail if a dispute arises later.

Your options once you have the lender's confirmation

Once you know the settlement figure, you have three options: walk away, which is simplest and lowest-risk if the seller won't cooperate; ask the seller to settle the finance first and proceed only once you hold the written settlement letter; or negotiate a price reduction and send the proceeds directly to the lender, with the seller receiving only the remainder.

Never hand over the full price on the promise that the seller will clear the finance afterwards. Sellers who make that promise rarely keep it, and once your money's gone, recovering it through the courts is slow, costly, and far from guaranteed.

Common scams and red flags to watch for

Used car fraud costs UK buyers tens of millions of pounds a year, and most victims skipped a car finance check before buying or ignored warning signs they'd already noticed. Spotting the patterns scammers use gives you a real advantage before you commit any money.

The "quick sale" pressure tactic

Artificial urgency is the most common manipulation tool in private car sales. A seller who insists the car will be gone by the end of the day, refuses to hold it for 24 hours while you run checks, or drops the price dramatically to push you into a same-day decision is almost certainly trying to prevent you from completing proper due diligence. Legitimate sellers understand that buyers need time to verify a vehicle, and they do not need to manufacture urgency to close a straightforward transaction.

If a seller's tone changes the moment you mention running a history check, treat that reaction as a serious warning rather than a minor inconvenience.

Walk away from any deal where the seller's timeline does not give you enough time to run a full report, inspect the V5C in person, and verify the VIN.

Signs the vehicle identity has been tampered with

Cloned and rung vehicles are cars that have had their registration plates or VIN switched to disguise a stolen vehicle or a write-off. These vehicles can pass a superficial inspection but will show discrepancies when you look closely. Watch for the following specific warning signs:

- VIN plates that show signs of being removed and refitted, such as tool marks around the edges or misaligned rivets

- Registration plates that do not match the font and spacing specified by DVLA regulations

- A V5C document reference number that does not appear on the DVLA's official records when you call to verify it on 0300 790 6802

- Mismatched paint finish around door sills or the engine bay, suggesting panel replacement after an accident

- A seller who arranged the viewing at a location other than the registered keeper's address shown on the V5C

Sellers who avoid putting things in writing

Any seller who refuses to communicate by email or text, insists on verbal-only agreements, or declines to send you photographs of the V5C and VIN before a viewing is removing your ability to create a documented record. Written evidence matters if the deal later turns into a legal dispute. Ask every seller to confirm key facts in writing, and treat a refusal as a clear signal that something in the deal does not hold up to scrutiny.

Quick recap

Running a car finance check before buying is not optional if you want to protect your money. Roughly one in three used cars carries outstanding finance, and the legal risk sits entirely with you the moment you hand over payment. Gather the registration plate and VIN first, verify the car through DVLA and DVSA tools, then run a full premium history report that bundles finance, stolen, and write-off data into a single result. Check the V5C in person, match the VIN physically, and run a second finance check on collection day before transferring any funds. If finance shows as outstanding, contact the lender directly and do not pay the seller until you have written confirmation that the debt is cleared.

Every step in this guide exists to close a gap that scammers rely on buyers leaving open. Start your check now with a full vehicle history report and see exactly what our reports cover before you buy.