Before Buying: How To Check If A Car Has Outstanding Finance

Avoid the risk of repossession. Learn how to check if a car has outstanding finance, identify hidden debt, and verify V5C logbooks before you buy.

Before Buying: How To Check If A Car Has Outstanding Finance

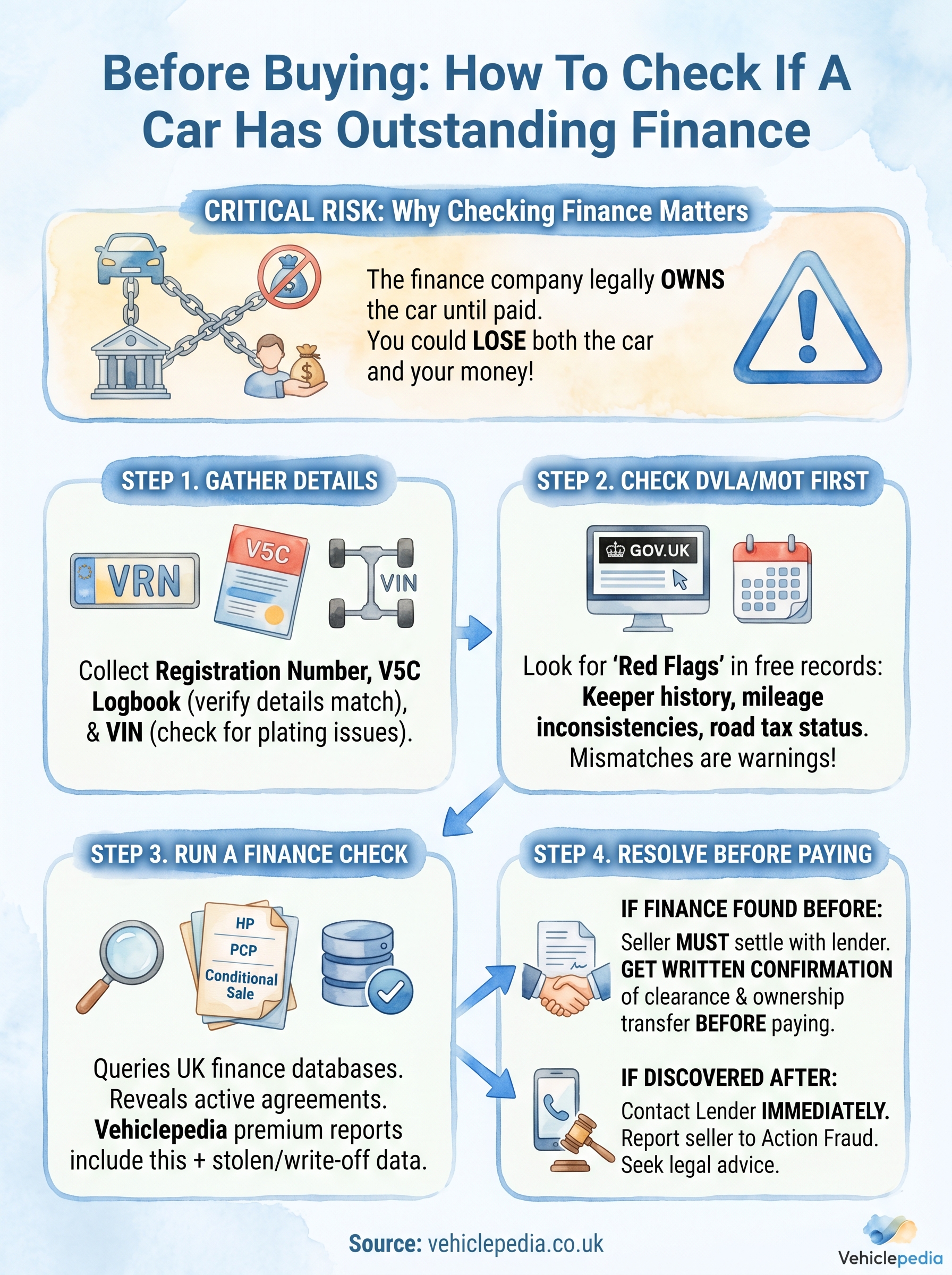

Buying a used car with outstanding finance attached is one of the most common, and costly, mistakes a buyer can make. If the previous owner still owes money on the vehicle, the finance company legally owns it, not the seller. That means you could lose both the car and your money, even if you bought it in good faith. Knowing how to check if a car has outstanding finance before you hand over any cash is essential.

The good news is that checking is straightforward, and you don't need any special access to do it. A finance check cross-references the vehicle against UK finance databases to reveal whether there's an active agreement tied to it. At Vehiclepedia, this is one of the key checks included in our premium vehicle history reports, alongside stolen vehicle and write-off data sourced directly from official registers.

In this guide, we'll walk you through exactly how finance on a car works, why it matters to you as a buyer, and the steps you can take to protect yourself. Whether you're buying privately or from a dealer, a few minutes of checking could save you thousands.

What outstanding finance means in the UK

In the UK, many cars are purchased through finance agreements rather than outright. The buyer pays monthly instalments to a lender, but until the final payment clears, the finance company holds legal ownership of the vehicle. This arrangement is standard and perfectly legal, but it creates a serious risk for anyone buying a used car without checking first.

How finance agreements work

When a seller takes out finance on a car, they get to use the vehicle, but they do not own it outright. The lender, typically a bank or specialist motor finance provider, retains a legal interest in the asset for the duration of the agreement. If the borrower sells the car while finance is still outstanding, they are selling something they don't legally own. That sale cannot transfer a clean title to you.

If you buy a car with outstanding finance attached, the finance company has the legal right to repossess it from you, regardless of what you paid.

What happens if you buy a car with finance on it

You can pay the full asking price in good faith and still lose the car. UK law does not protect private buyers in the same way it protects those who buy from a dealer in certain circumstances. Your only practical recourse is to pursue the seller for your money, which is often difficult if they've disappeared or lack funds. This is exactly why knowing how to check if a car has outstanding finance before any money changes hands is so important.

The most common finance types to watch for

Most UK car finance falls into one of three categories. Each one keeps legal ownership with the lender until the debt is cleared:

- Hire Purchase (HP): The lender owns the car until the final payment

- Personal Contract Purchase (PCP): Ownership only transfers if you pay the optional final balloon payment

- Conditional Sale: Similar to HP, with ownership held by the lender throughout the term

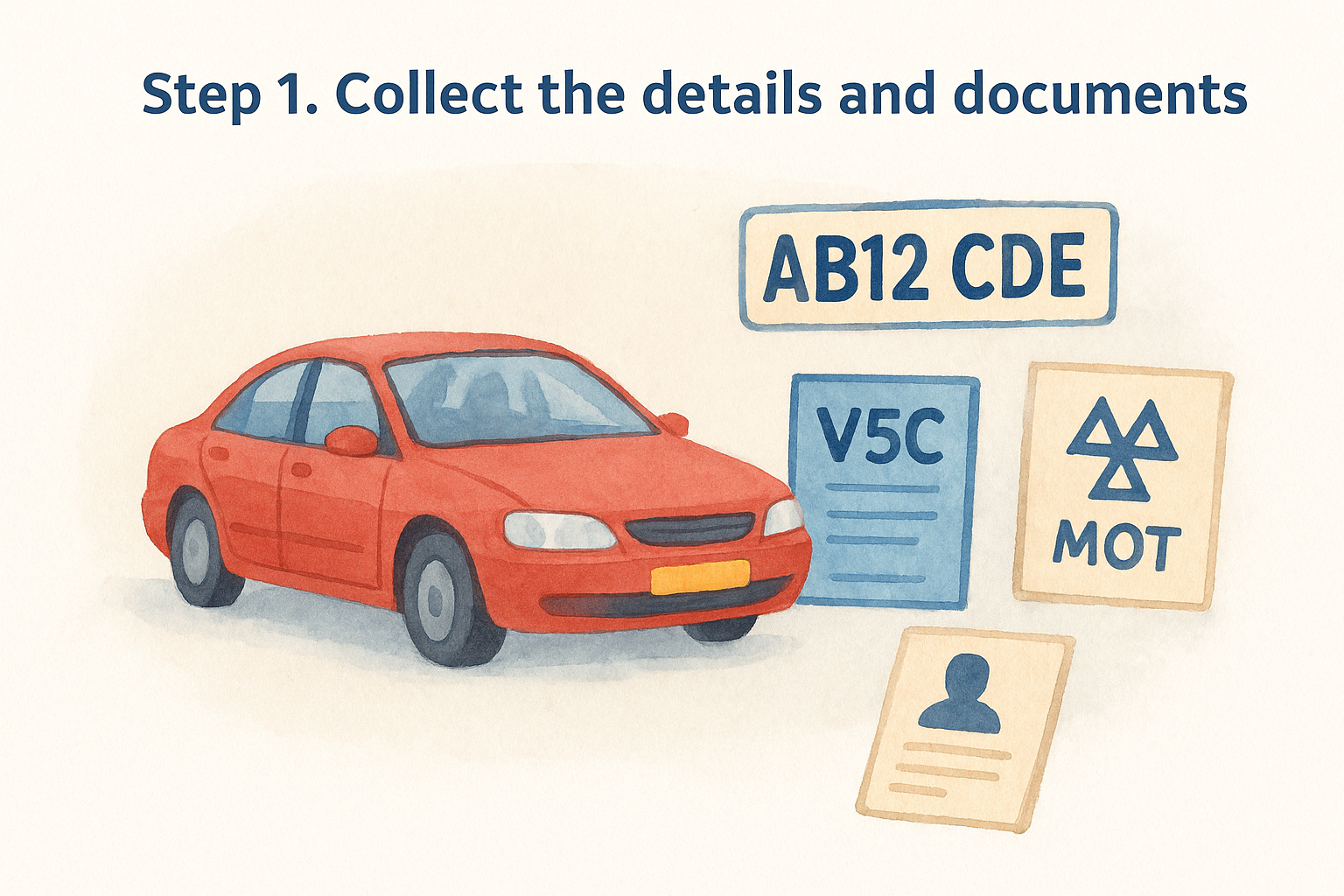

Step 1. Collect the details and documents

Before you run any kind of check, you need to gather the right information about the vehicle. Having everything in one place means you can move through the process quickly and spot any inconsistencies between documents that might signal a problem early on.

What to gather before you start

The most important item is the vehicle registration number, which appears on the number plate. You'll also need the V5C logbook (the vehicle's registration certificate) if the seller has it available. Cross-referencing both ensures the registration number matches the logbook details, which is a basic but important step when you're learning how to check if a car has outstanding finance.

Never hand over money before you've physically seen and checked the V5C in person.

Collect the following before moving to any online checks:

| Document or Detail | Why You Need It |

|---|---|

| Registration plate number | Required for all database checks |

| V5C logbook | Confirms registered keeper and vehicle details |

| VIN (chassis number) | Lets you verify the car hasn't been re-plated |

| Seller's name and contact details | Needed if you need to pursue them later |

| MOT certificate (if available) | Cross-checks mileage and vehicle condition history |

Step 2. Check DVLA and MOT records first

Before running a finance-specific check, it's worth looking at free DVLA and MOT history records first. These checks won't directly answer how to check if a car has outstanding finance, but they help you spot wider red flags that might indicate a problematic vehicle before you spend money on a premium report.

What to look for in the DVLA records

The DVLA holds the official registered keeper history for every vehicle in the UK, along with road tax status and basic vehicle data. You can check make, colour, and engine size for free on the GOV.UK website. Pay close attention to whether the number of previous keepers matches what the seller tells you. Frequent keeper changes or unexplained gaps in the history can be a warning sign worth pressing the seller on.

A mismatch between the seller's account and the official DVLA data is a reason to stop and ask questions before going any further.

What MOT history tells you

MOT history records every mileage reading taken at each test, which lets you spot inconsistencies over time. A sudden drop in recorded mileage between tests is a strong indicator of clocking. You can access the full MOT history for free directly through the official GOV.UK vehicle enquiry service.

Step 3. Run an outstanding finance check

This is the most direct way to find out if a car carries active debt. A dedicated finance check queries the UK's main finance databases and returns a clear result showing whether the vehicle has any outstanding agreements registered against it. This is the core step when you want to know how to check if a car has outstanding finance.

What the check covers

A finance check searches across major UK lending registers, including HP, PCP, and conditional sale agreements. At Vehiclepedia, our premium report pulls this data alongside stolen vehicle and write-off records, giving you a complete picture in one place rather than running multiple separate searches.

A clean finance result doesn't guarantee the car is entirely problem-free, but it removes one of the biggest legal risks you face as a buyer.

What to look for in the results

Your report will clearly show whether any finance agreement is active or settled. If finance shows as outstanding, check the following before you go any further:

- The lender's name, which confirms who legally owns the vehicle

- The agreement type (HP, PCP, or conditional sale)

- Whether the seller has confirmed the outstanding balance directly with the lender

Step 4. Resolve issues before or after purchase

Finding active finance on a vehicle doesn't mean the deal is dead. What matters is how you handle the information and whether the seller is willing to cooperate before any money changes hands.

If finance shows as outstanding before you buy

The safest route is to ask the seller to settle the finance directly with the lender before the sale completes. Get written confirmation from the lender that the agreement is cleared and that legal ownership has transferred to the seller. If the seller refuses or can't provide this, walk away. No discount is worth the risk of losing the car to repossession after you've paid.

Never accept a seller's verbal assurance that the finance "will be sorted" after you pay. Get written proof from the lender before you hand over anything.

Ask the lender to confirm the following in writing:

- A signed settlement confirmation letter

- The exact date the agreement closed

- Confirmation that no further sums are owed on the vehicle

If you discover finance after you've already paid

This situation is harder, but you do have options. Contact the lender directly to explain you purchased the vehicle without knowing about the outstanding agreement, then report the seller to Action Fraud and seek legal advice on recovering your money. Running a check on how to check if a car has outstanding finance before you pay is always the better path, and this outcome is exactly why that step matters.

Next steps

Checking for outstanding finance is one of the most important steps you can take before buying a used car in the UK. If you've followed this guide, you now know how to check if a car has outstanding finance, what the results mean, and how to act if something shows up before or after you pay.

Your next move is to run the check before you commit to anything. Vehiclepedia's premium report covers finance, stolen vehicle status, and write-off data in a single search, all drawn from official UK databases. You can view a sample report before you buy to see exactly what you'll receive.

Skipping this check is the one mistake you can easily avoid. A few minutes of straightforward verification now could save you from losing both your car and your money to a finance company that has every legal right to repossess it.