Can You Sell A Car With Outstanding Finance? UK Options

Can you sell a car with outstanding finance? Learn how to settle HP/PCP debt, get a settlement figure, and sell your car legally and safely in the UK.

Can You Sell A Car With Outstanding Finance? UK Options

If you're wondering can you sell a car with outstanding finance, the short answer is yes, but not without settling the debt first. The finance company technically owns the vehicle (or holds a legal interest in it) until every penny is paid off, which means selling without clearing the balance could land you in serious legal trouble, including fraud charges.

The good news is that thousands of UK car owners do this every year, and there are clear, legitimate routes to make it happen. Whether you're selling privately, trading in at a dealership, or using a car-buying service, each option handles the outstanding finance differently, and some are far simpler than others.

This guide walks you through every step, from getting a settlement figure to completing the sale legally. Before listing any car for sale, it's worth running a vehicle history check through Vehiclepedia to confirm exactly what finance (if any) is registered against it, the same check a savvy buyer will almost certainly run themselves.

What outstanding finance means in the UK

When you take out car finance in the UK, the lender typically retains a legal interest in the vehicle until you clear the balance. That means even though you drive the car every day and your name appears on the V5C logbook, the finance company holds enforceable rights over that asset. Selling the vehicle without their knowledge or without settling the debt first is not just a contractual breach; it can constitute fraud under UK law, exposing you to criminal liability.

Who actually owns the car?

The V5C logbook records you as the registered keeper, not the legal owner. This distinction catches a lot of people off guard. With most finance agreements, the lender remains the legal owner until the final payment clears. If you sell the car to a private buyer who runs a vehicle history check before handing over money, that check will flag the outstanding finance. The buyer would have no legal right to keep the car, even after paying you in full, because the finance company's interest takes priority.

A private buyer who discovers registered finance can pursue a full refund from you through the courts, and many do.

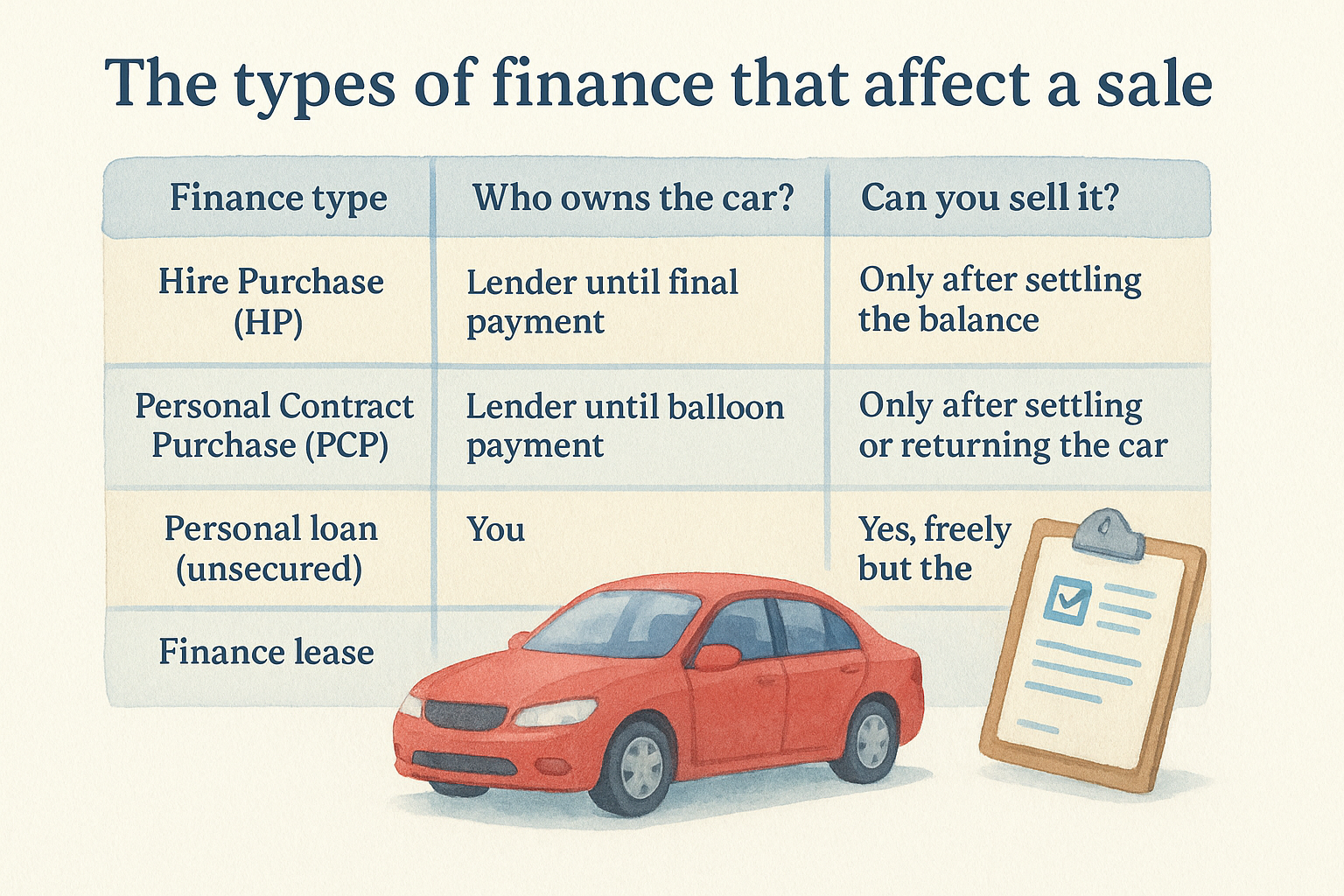

The types of finance that affect a sale

Not every finance agreement works the same way, and the type you hold directly shapes your options when you want to sell. Here is a quick breakdown of the most common agreements you will encounter:

| Finance type | Who owns the car? | Can you sell it? |

|---|---|---|

| Hire Purchase (HP) | Lender until final payment | Only after settling the balance |

| Personal Contract Purchase (PCP) | Lender until balloon payment | Only after settling or returning the car |

| Personal loan (unsecured) | You | Yes, freely, but the loan still exists |

| Finance lease | Lender throughout | Generally no; contact your lender first |

With a personal loan, the bank lent you money with no charge registered over the vehicle, so you can sell freely without their consent. The loan itself still runs independently and you still owe every penny. With HP or PCP, the lender holds a formal charge that will appear on any finance history check. This is exactly why answering the question of whether you can sell a car with outstanding finance begins with identifying which agreement you actually signed.

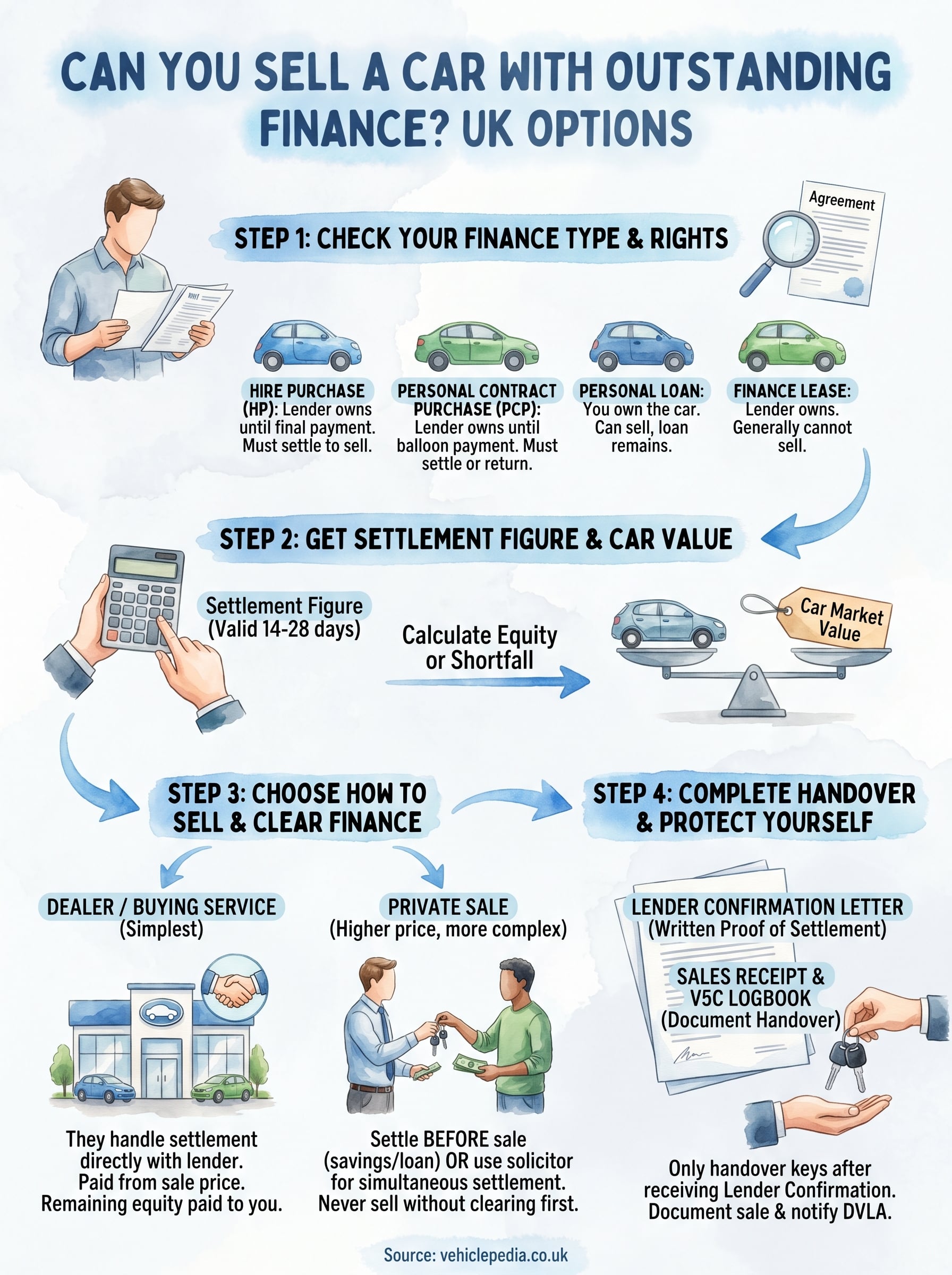

Step 1. Check your finance type and rights

Before you can answer the question of whether you can sell a car with outstanding finance, you need to know exactly what type of agreement you signed. Pull out your original finance paperwork or log into your lender's online portal. Look for the agreement type on the first page; it will say Hire Purchase (HP), Personal Contract Purchase (PCP), Personal Loan, or Finance Lease in clear terms.

Find your agreement documents

If you cannot locate the physical paperwork, contact your lender directly and ask them to confirm the agreement type in writing. Your lender is legally required to supply you with a copy of your credit agreement under the Consumer Credit Act 1974, so do not be put off if the original documents are long gone. Most lenders will email a summary within a few working days.

Here is what to look for on the first page of your agreement:

- Agreement type: HP, PCP, Personal Loan, or Finance Lease

- Lender name and contact details

- Total amount payable and the outstanding balance section

- Term length and the date your agreement started

Write down the lender name, account reference, and agreement type before moving to the next step, as you will need these details repeatedly throughout the process.

Understand what rights you have

Your rights vary significantly depending on the agreement. Under a PCP or HP deal, you have no right to sell the vehicle until the finance is settled, because the lender holds a legal charge over it. With a personal loan, you own the car outright and can sell freely, though the loan repayments continue independently. Check whether your agreement includes a voluntary termination clause under Section 99 of the Consumer Credit Act 1974, which lets you hand the car back if you have already paid 50% or more of the total amount payable.

Step 2. Get a settlement figure and value the car

Once you know your agreement type, the next move is to find out exactly how much you owe and what your car is worth. These two numbers determine whether you can sell a car with outstanding finance and walk away without any shortfall to cover yourself.

Request your settlement figure

Your lender is legally required to provide a settlement figure within seven working days under the Consumer Credit Act 1974. Call or log into your lender's online portal and ask for an early settlement quote in writing. Most lenders will email one within 24 to 48 hours. The figure is only valid for a fixed period, typically 14 to 28 days, so time any sale accordingly.

Request a fresh settlement figure if more than 14 days pass, as interest accrues daily and the amount will change.

Here is a straightforward template you can send directly to your lender:

Subject: Early Settlement Quote Request

Dear [Lender Name],

I am writing to request an early settlement figure for my finance agreement, reference number [XXXXXX]. Please confirm the total amount required to settle the agreement in full and the date until which this figure remains valid.

Kind regards,

[Your Name]

Value your car accurately

Run valuations across at least two or three sources to build a realistic picture of your car's market value. Look at what comparable vehicles with similar mileage and condition are actually selling for in your area, not just listed at. The difference between your car's value and your settlement figure tells you immediately whether you hold positive equity or whether you face a shortfall that needs covering before the sale can complete.

Step 3. Choose how to sell and clear the finance

Once you have your settlement figure and car value, you can pick the best route. The method you choose directly affects how the finance gets cleared, so understanding each option matters if you want to answer can you sell a car with outstanding finance without complications.

Selling to a dealer or car-buying service

Dealers and car-buying services handle outstanding finance settlements routinely, making them the simplest option. When you agree a price, the buyer contacts your lender directly, pays the settlement figure to the finance company, and transfers any remaining equity to you. You hand over the keys once everything is confirmed.

Always get written confirmation that the dealer has contacted your lender and requested the settlement before you sign anything.

Here is how the process typically flows:

- Agree a sale price with the dealer or buying service

- Provide your lender name and account reference

- Dealer requests your settlement figure directly

- Dealer pays the lender the settlement amount

- Remaining equity (if any) is paid to you

Selling privately

Private sales typically achieve higher prices than dealer routes, but they demand more care when outstanding finance is involved. You must settle the finance before or simultaneously with the sale, never after. The safest approach is to use a solicitor to hold the buyer's funds in escrow, pay the lender directly, and release the remaining balance once the finance company confirms the debt is cleared.

A common alternative is to pay off the settlement figure yourself before listing the car, using savings or a short-term loan to clear the balance first. This removes the complication entirely and lets you sell as a private owner with no registered finance, which makes the car far easier to market.

Step 4. Complete the handover and protect everyone

The final step is where most mistakes happen. Even if you have settled the outstanding finance correctly, handing over the car without proper documentation leaves both you and the buyer exposed. This stage is especially important if you are answering the question can you sell a car with outstanding finance, because proving the debt was cleared before the sale protects you from any future dispute.

Get written confirmation from your lender

Once the finance company receives full payment, request a settlement confirmation letter in writing before you hand over the keys. Most lenders issue this by email within one to three working days. Do not proceed with the handover until you hold this document in your hands, as it proves the lender's interest in the vehicle has ended.

Keep a digital copy of this letter permanently, as a buyer could raise a dispute months after the sale.

Document the sale properly

A written receipt protects both parties and serves as evidence if any disagreement arises later. Use the template below for a private sale:

Vehicle Sale Receipt

Date of sale: [DATE]

Seller full name: [NAME]

Buyer full name: [NAME]

Vehicle registration: [REG]

Make and model: [MAKE / MODEL]

VIN: [VIN]

Agreed sale price: £[AMOUNT]

Finance settlement confirmed: Yes / No

Settlement reference number: [REF]

Both parties confirm the vehicle is sold as seen and the seller holds no outstanding finance against it at the point of sale.

Seller signature: ________________

Buyer signature: ________________

Hand over the V5C logbook at the same time, and notify the DVLA of the change of keeper immediately using the yellow slip or the online service.

Key takeaways before you sell

Selling a car with outstanding finance is legal in the UK, but only if you settle the debt before or during the sale. The finance company holds a legal interest in the vehicle until you clear the balance, so handing over the keys without dealing with that first puts both you and your buyer at risk. Know your agreement type, get your settlement figure in writing, and confirm your car's value before you commit to any sale route.

Dealers and car-buying services handle the settlement process for you, which makes them the lowest-friction option. Private sales can return more money but require either paying off the balance beforehand or using a solicitor to manage the funds safely. Whatever route you take, always collect a written settlement confirmation from your lender before the handover.

Before you list the car, run a full check through Vehiclepedia's sample report to see exactly what a buyer will find, and get ahead of any surprises.