What Happens When A Car Is Written Off In The UK?

Learn what happens when a car is written off in the UK. Understand insurance categories, negotiate fair settlements, and discover your salvage options.

What Happens When A Car Is Written Off In The UK?

Getting a call from your insurer to say your car has been declared a total loss is never welcome news. But understanding what happens when a car is written off can make the difference between a fair outcome and one that leaves you out of pocket. From the moment your insurer decides repairs aren't economically worthwhile, a specific process kicks in, covering everything from how your settlement is calculated to what happens to the vehicle itself.

Whether you've been in an accident, experienced flood damage, or had your car stolen and recovered, the steps that follow a write-off affect your finances, your legal obligations, and your next vehicle purchase. This guide walks you through the entire write-off process in the UK, including insurance categories, settlement negotiations, and your rights as a vehicle owner. We'll also cover how to protect yourself when buying a replacement, something a vehicle history check through Vehiclepedia can help with, by flagging previously written-off cars before you commit to a purchase.

What 'written off' means and the UK categories

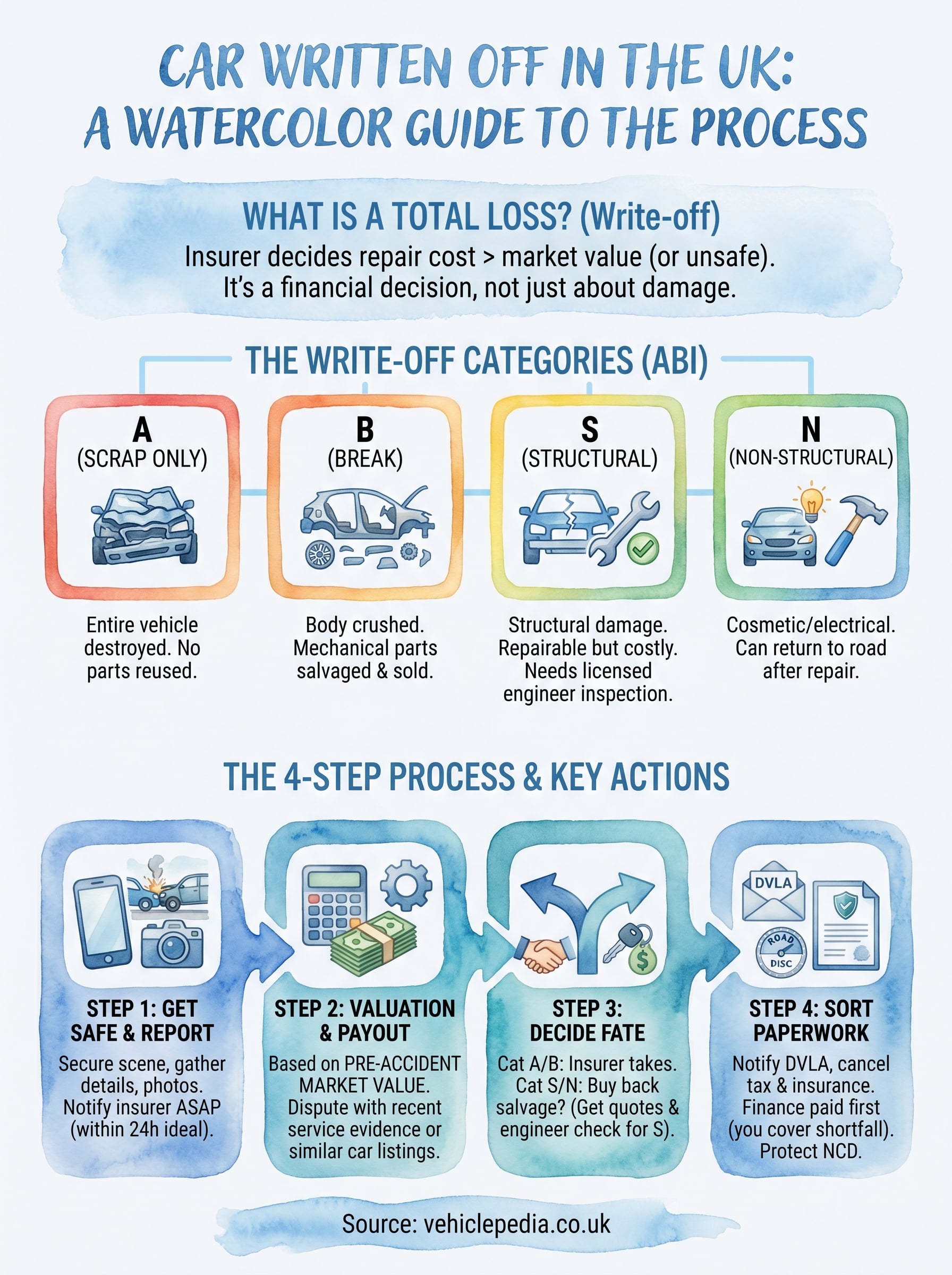

A car is declared a total loss (commonly called a "write-off") when your insurer decides the cost of repairing it exceeds its market value, or when the damage makes it unsafe to return to the road. This is a purely financial calculation on your insurer's part, and it happens more often than most drivers expect. Understanding what happens when a car is written off starts here, because the category your insurer assigns determines everything from what the insurer pays you to whether the vehicle can ever legally drive again.

A write-off declaration doesn't automatically mean your car is beyond repair. It means your insurer has decided repairs aren't financially worthwhile.

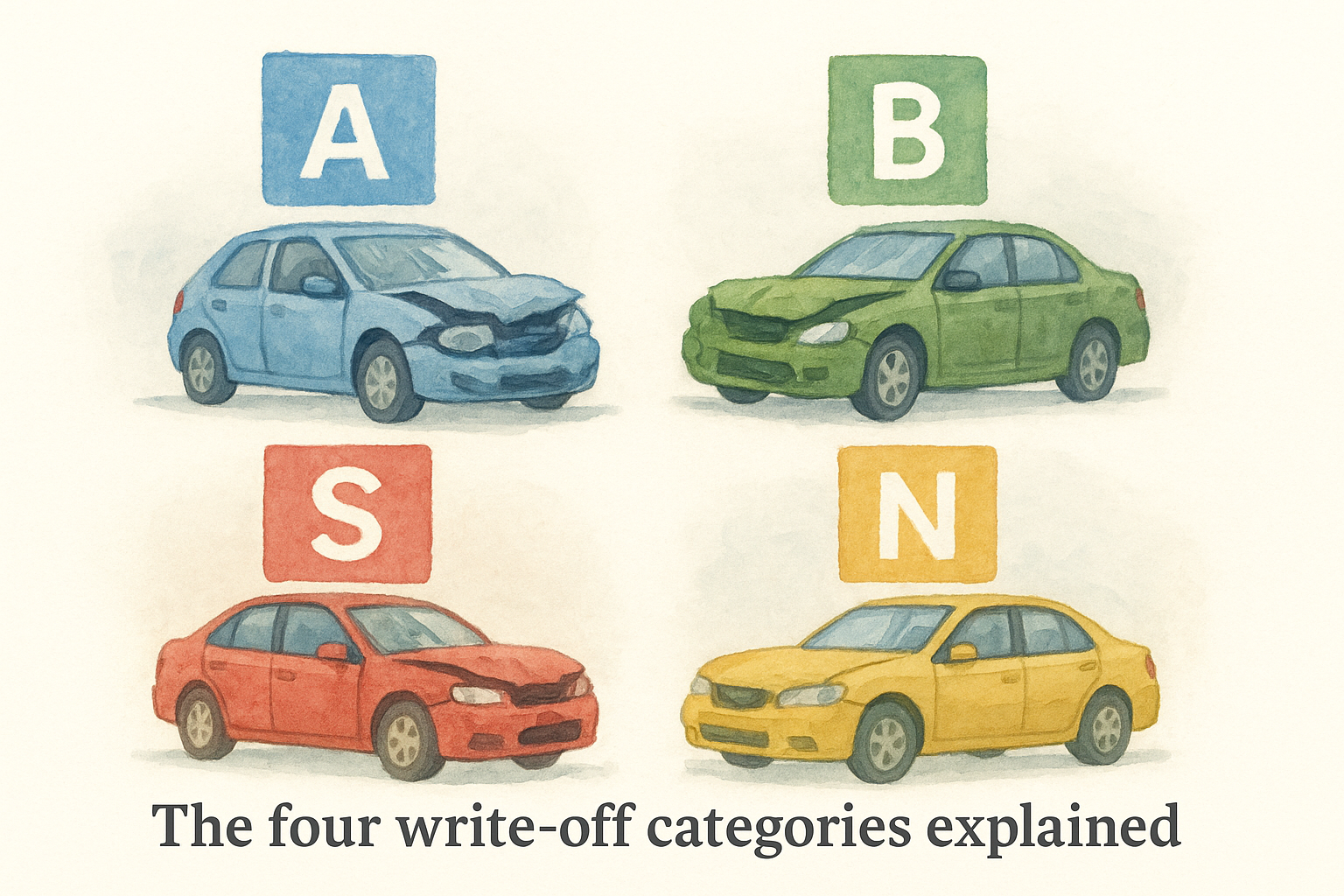

The four write-off categories explained

The Association of British Insurers (ABI) divides written-off vehicles into four categories. Each category carries specific rules about what can happen to the car after it's declared a total loss. Knowing your category is the first piece of actionable information you need, so ask your insurer to confirm it in writing as soon as they make the decision.

| Category | What it means | Can it return to the road? |

|---|---|---|

| A | Scrap only. The entire vehicle must be crushed and no parts can be reused. | No |

| B | The body shell must be crushed, but mechanical parts can be salvaged and sold. | No |

| S (formerly Cat C) | Structural damage. Repair is technically possible but costs more than the car's value. | Yes, after professional repair and inspection |

| N (formerly Cat D) | Non-structural damage such as electrical or cosmetic faults. Repair cost exceeds value. | Yes, after repair |

What Cat S and Cat N mean in practice

Categories S and N are the ones most likely to affect you as a buyer or seller of a used car, and both carry lasting consequences. A Cat S vehicle must pass an inspection by a licensed engineer before it can be re-registered with the DVLA, while a Cat N car can legally return to the road without a structural check. Both categories must be recorded on the V5C logbook, and both will reduce the car's resale value, sometimes by a significant margin.

Step 1. Get safe and start the claim

Before you think about insurance categories or settlement figures, your first priority is physical safety. If you've been in a collision, move to a safe location if possible, switch on your hazard lights, and call emergency services if anyone is injured. Understanding what happens when a car is written off begins long before your insurer makes a decision; it starts at the scene.

Secure the scene and gather evidence

Documenting the damage thoroughly at this stage gives you real leverage later in the claims process. Take clear photographs of all four sides of the vehicle, any damage to other vehicles or property, road conditions, and any visible debris. Collect the details listed below before you leave the scene.

- Full name, address, and phone number of all parties involved

- Insurance details (insurer name and policy number) from other drivers

- Vehicle registration numbers for all vehicles present

- Names and contact details of any witnesses

- A reference number if police attended

Notify your insurer promptly

Contact your insurer as soon as possible, ideally the same day. Most policies require you to report an incident within 24 hours, and delaying can affect your claim.

When you call your insurer, stick strictly to the facts. Avoid speculating about fault or estimated repair costs, as anything you say can influence how your claim is assessed.

When your insurer picks up, confirm the vehicle's location, state whether it is driveable, and provide your policy number. They will arrange an independent engineer to inspect the vehicle and decide whether it qualifies as a total loss.

Step 2. Understand the valuation and payout

Once your insurer's engineer confirms the write-off, the next stage of what happens when a car is written off is the settlement offer. Your insurer will calculate the car's pre-accident market value (not what you originally paid for it, and not the cost of a brand-new equivalent) and make you an offer based on that figure.

You are not obligated to accept the first offer. If you believe the valuation is too low, you have every right to challenge it with evidence.

How insurers calculate market value

Your insurer will typically use classified listing data from used car platforms to establish what your vehicle was worth immediately before the incident. Factors such as mileage, service history, age, and condition all feed into that figure, so gather any evidence that supports a higher valuation before you respond.

Recent maintenance work can strengthen your position considerably. If your car had new tyres, a full service, or a fresh MOT in the months before the incident, provide the receipts to your insurer as supporting evidence alongside your response to their offer.

How to dispute a low offer

Challenging a valuation is straightforward if you gather comparable listings for similar vehicles. Search for cars of the same make, model, year, mileage, and specification currently advertised for sale. Screenshot at least three examples and submit them to your insurer in writing.

- Include the listing URL, advertised price, mileage, and specification for each example

- State clearly that you are disputing the settlement figure

- Request a written response within seven to ten working days

Step 3. Decide what happens to the car

Once you accept your settlement, your insurer will typically take ownership of the vehicle. This is the point in what happens when a car is written off where you face a key decision: whether to let the insurer sell the salvage or to buy it back yourself.

Keep the salvage or hand it over

If the car falls into Category A or B, you have no choice: the insurer must ensure it is destroyed, and you cannot retain it. For Category S or N vehicles, you have the option to buy back the salvage from your insurer, usually at a set amount deducted directly from your settlement payout.

Buying back salvage can make financial sense if repairs are genuinely cheaper than the deduction, but get written quotes from qualified mechanics before you commit to anything.

What to do if you keep a Cat S or Cat N car

Keeping a written-off vehicle comes with clear legal responsibilities that you must follow before putting the car back on the road. A Cat S car must be inspected and signed off by a licensed engineer before you can re-register it with the DVLA. A Cat N car has no mandatory structural inspection, but you must still declare its write-off status on the V5C logbook when you re-register it.

- Get at least two written repair quotes from qualified garages before agreeing to the salvage deduction

- Ask your insurer to confirm the exact salvage buy-back figure in writing

- Book a vehicle inspection for any Cat S car before you arrange re-registration with the DVLA

Step 4. Sort DVLA, tax, finance and insurance

Once your settlement is agreed and the vehicle's fate is decided, the final part of what happens when a car is written off is sorting the paperwork correctly. Getting this right protects you from unexpected bills and legal complications you did not see coming.

Notify the DVLA and reclaim your road tax

You must inform the DVLA that your vehicle has been written off. If your insurer takes ownership, they handle the DVLA notification, but confirm this in writing so you have a clear record. If you have sold or scrapped the car yourself, complete the relevant section of the V5C logbook and send it to the DVLA without delay.

Cancel your road tax as soon as the car leaves your possession, because the DVLA will automatically refund any full months remaining on your Vehicle Excise Duty.

Clear any outstanding finance

Outstanding finance on a written-off vehicle does not disappear. If you have a Personal Contract Purchase (PCP) or hire purchase agreement, your insurer pays the finance company first, not you directly. Check your settlement figure against the remaining balance; if there is a shortfall, you are legally responsible for covering it. GAP insurance exists specifically to bridge this difference, so check your policy documents now.

Update your insurance

Cancel or transfer your existing policy as soon as the car is no longer in your name. Notify your insurer in writing and request written confirmation of your no-claims bonus so you can carry it forward to your next policy without dispute.

A quick recap and what to do next

Understanding what happens when a car is written off comes down to four clear steps: report the incident and gather evidence, challenge the valuation if it falls short, decide whether to keep or hand over the salvage, and sort your DVLA notification, finance, and insurance without delay. Each step has real financial and legal consequences, so skipping any one of them can cost you money or create problems you did not anticipate.

Your next vehicle purchase carries its own risk, particularly if you are looking at used cars. A previously written-off car may look perfectly fine on the outside but carry hidden structural damage or an outstanding finance agreement. Before you hand over any money, run a full vehicle history check to see exactly what a car has been through, including any write-off category recorded against it. View a sample Vehiclepedia report to see what information is available before you buy.